Individual Taxpayer Identification Number (ITIN)

WHAT IS AN ITIN?

An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the U.S. Internal Revenue Service (IRS). An ITIN consists of nine digits, beginning with the number nine (i.e., 9XX-XX-XXXX). Since 1996, the IRS has issued ITINs to taxpayers and their dependents who are not eligible to obtain a Social Security number (SSN).

As a result of a new law and as discussed below, many ITINs will expire and need to be renewed.

WHY DOES THE IRS ISSUE ITINs?

All wage earners—regardless of their immigration status—are required to pay federal taxes. The IRS provides ITINs to people who are ineligible for an SSN so that they can comply with tax laws.

WHO USES AN ITIN?

Taxpayers who file their tax return with an ITIN include undocumented immigrants and their dependents as well as some people who are lawfully present in the U.S., such as certain survivors of domestic violence, Cuban and Haitian entrants, student visa–holders, and certain spouses and children of individuals with employment visas. As of August 2012, the IRS had assigned 21 million ITINs to taxpayers and their dependents.

Once a person who has been issued an ITIN is eligible to apply for an SSN, the person may no longer use the ITIN.

WHAT IS AN ITIN USED FOR?

ITINs are issued by the IRS specifically as a means to pay federal taxes. While the IRS issues them solely for this purpose, ITINs may sometimes be accepted for other purposes, such as for opening an interest-bearing bank account, in employment dispute settlements, or for obtaining a mortgage.

WHY DO UNDOCUMENTED IMMIGRANTS NEED AN ITIN?

In addition to being required to pay taxes, immigrants benefit from filing income tax returns because:

- It demonstrates that they are complying with federal tax laws.

Filing federal taxes is a way for immigrants to further contribute to the economy. - It is one way that people who may have an opportunity to legalize their immigration status and become U.S. citizens can prove that they have “good moral character.”

- Immigrants can use tax returns to document their work history and physical presence in the U.S. In order to be eligible for legal immigration status under any future immigration reform, people who currently are unauthorized to be in the U.S. most likely will have to be able to prove that they have been employed and have lived continuously in the U.S. for a certain number of years.

- People who file tax returns can claim crucial economic supports, such as the Child Tax Credit, including the refundable portion (also known as the Additional Child Tax Credit).

- Filing a tax return is required in order to be able to claim insurance-premium tax credits for family members—often U.S. citizen children—who are eligible for health care coverage under the Affordable Care Act (ACA, or “Obamacare”). These tax credits are necessary to help make health insurance affordable to people who otherwise would not be able to buy it.

- Individuals who are eligible to file their taxes with an ITIN can establish that they are eligible for an exemption from the ACA’s individual mandate, which requires that people have health insurance. Undocumented immigrants are excluded from all ACA benefits, so they are not eligible to buy health insurance through the ACA’s health care marketplace, even at full cost.

- Immigrant workers who receive settlement payments as a result of an employment-related dispute will be subject to the maximum tax withholding rate, unless they have an ITIN. For example, for a worker with an ITIN, the withholding on back wages paid to the worker because of a settlement will be based on the worker’s family status and the number of exemptions the worker can claim. By contrast, if the worker did not have an ITIN, the withholding would be figured as if the worker were single with no exemptions. Similarly, for workers without ITINs, the withholding on payments other than wages, e.g., on payments for punitive damages, is figured at the “backup withholding” rate of 28 percent, whereas workers who have ITINs ordinarily would have no withholding on such non-wage payments.

WHAT IS AN ITIN NOT USED FOR?

An ITIN does not authorize a person to work in the U.S. or provide eligibility for Social Security benefits. An ITIN does not provide a person with immigration status.

DO ITIN-FILERS PAY INCOME TAXES?

Yes! In 2010, over 3 million federal tax returns were filed with ITINs, which accounted for over $870 million in income taxes. In the same year, over 3 million unauthorized workers, including ITIN-filers, paid over $13 billion into Social Security.

IS IT SAFE TO USE AN ITIN?

Generally, yes. The IRS has strong privacy protections in place to ensure that immigrants who report their income and file their taxes are not at risk of having their information shared. Under Internal Revenue Code section 6103, the IRS is generally prohibited from disclosing taxpayer information, including to other federal agencies. However, certain exceptions apply. For example, the IRS is required to disclose taxpayer information to certain U.S. Treasury Department employees when they request it for tax administration purposes or to other federal agencies if it’s needed for a non-tax criminal investigation and a federal court has ordered that it be provided.

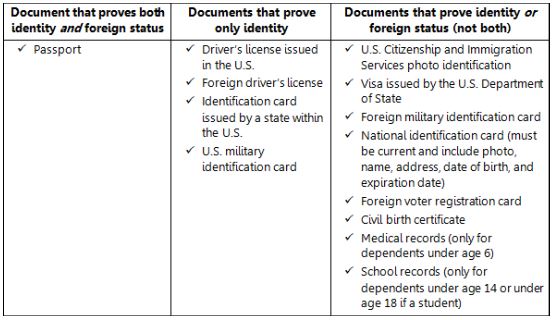

WHAT DOCUMENTS MUST A PERSON PRESENT WHEN APPLYING FOR AN ITIN?

ITIN applicants are required to provide proof of their identity, foreign nationality status, and residency. (Proof must be submitted that any applicant claimed as a dependent resides in the U.S., unless they are from Mexico or Canada or are a dependent of U.S. military personnel stationed overseas.) In 2015, Congress codified the severe restrictions that the IRS had put in place on the types of documents that new ITIN applicants may present.

In order to apply for an ITIN, the applicant must

1. complete a Form W-7, Application for IRS Individual Taxpayer Identification Number, along with their federal income tax return, and

2. prove their identity and foreign nationality status by providing a combination of original documents (see the table below) or certified copies of the documents. (A certified copy is one that the original issuing agency provides and certifies as an exact copy of the original document and that contains an official stamped seal from that agency. Notarized copies are not acceptable.)

The IRS will accept only a combination of the 13 documents listed in the table below as proof of identity and/or foreign nationality status. Applicants who can present a passport have to present only one document. Otherwise, they will need to present at least two documents or certified copies of at least two documents.HA

How does an applicant file for an ITIN?

Tax Partners is a Certified Acceptance Agent (CAA) authorized by the IRS. We can do this for you completely without having to mail or in person to an IRS employee or a designated U.S. diplomatic mission or consular post.

An applicant can also apply for an ITIN by mail, in person through a designated IRS Taxpayer Assistance Center (TAC), or with the help of an Acceptance Agent (AA) or a Certified Acceptance Agent (CAA) authorized by the IRS. An applicant who resides outside the U.S. may apply by mail or in person to an IRS employee or a designated U.S. diplomatic mission or consular post.

Applicants who apply for an ITIN by mail directly with the IRS must submit either the original of each supporting document or a certified copy of each supporting document. Applicants who do not want or are unable to mail their original documents or certified copies to the IRS may take them in person to a TAC or CAA to have the documents (or certified copies) verified and immediately returned to them. However, not all TACs provide ITIN-related services, or they may provide them only during restricted business hours. Because the number of TACs and CAAs is limited, many ITIN applicants simply aren’t able to take their applications and documents to a TAC or CAA.

As of 2016, CAAs are allowed to authenticate the passport and birth certificate for dependents (though not other forms of acceptable identity documents). For primary and secondary applicants, CAAs are authorized to authenticate all 13 forms of acceptable identification documents. TAC offices are authorized to authenticate only the passport, birth certificate, and foreign national ID cards for ITIN applicants (including for dependents).

How long does it take to receive an ITIN?

Outside of peak processing times (between January and April), it should take up to ten weeks for an applicant to receive their ITIN. However, because most ITIN applications must be filed with tax returns, they are typically filed during peak processing times. As a result, it can take 12 to 15 weeks to receive an ITIN. Any original documents or certified copies submitted in support of an ITIN application will be returned within 65 days. People who do not receive their original and certified documents within 65 days of mailing them to the IRS may call 1-800-908-9982 to check on their documents’ whereabouts.

After the ITIN application has been approved, the IRS will process the tax return within 12 to 16 weeks.

Who processes ITIN applications?

All ITIN applications are processed by the ITIN unit in the IRS Submission Processing Center in Austin, Texas. Tax returns attached to the ITIN applications are “sent for processing.” Tax examiners in the ITIN unit review ITIN applications and supporting documentation. Based on the tax examiner’s review, the application will be either:

assigned — the IRS mails a notice with the assigned ITIN to the applicant;

rejected — the IRS mails a notice informing the applicant (a) that the ITIN application was rejected, (b) the reason for the rejection and (c) that the applicant must file another application to reapply for an ITIN; or

suspended — the ITIN application is suspended because of a procedural issue or because it has questionable information. (IRS guidelines define a questionable application as one for which the tax examiner identifies one or more discrepancies on the application. A procedural issue is one in which the applicant did not properly complete the application or did not attach the required documentation to the application.)

How long is an ITIN valid?

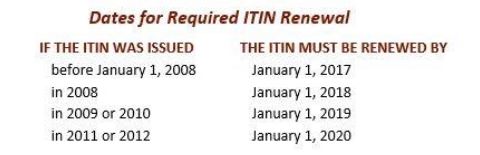

ITINs previously were issued for an indefinite period. In 2015, Congress mandated that people who received ITINs prior to January 1, 2013, are required to renew their ITINs on a staggered schedule between 2017 and 2020 (see the table below). In addition, the new law states that an ITIN will expire if the person to whom it was issued fails to file a tax return for three consecutive years.

An ITIN issued after December 31, 2012, will remain valid unless the person to whom it was issued does not file a tax return—or is not included as a dependent on the return of another taxpayer—for three consecutive years.

Who needs to renew their ITIN?

Two categories of ITINs expired on January 1, 2017:

1. any ITIN not used to file a tax return for the last three years (2013, 2014, or 2015)

2. ITINs with middle digits 78 or 79 (i.e., 9XX-78-XXXX and 9XX-79-XXXX)

According to the IRS, the agency sent notification letters in August and September 2016 to all individuals whose ITINs had the middle digits 78 and 79 “that were currently being used on a tax return,” informing them that their ITIN would expire on January 1, 2017. Anybody who needs and wants an ITIN to file their taxes and whose ITIN expired on January 1, 2017, must apply to renew their ITIN.

What are the barriers to getting an ITIN?

Because ITIN applicants face many difficulties obtaining certified copies of their identity documents, and because of the limited options for in-person verification of these documents, many ITIN applicants may be forced into the vulnerable position of going without valuable identity documents for weeks or months (or longer, if their documents are lost). For some, this has proven too risky and burdensome.

As a result, the ITIN rules that went into effect in 2012 caused a dramatic decline in the number of ITIN applications. In 2013, there were nearly 50 percent fewer ITIN applications than in each of the previous three years. In addition, the IRS rejected over 50 percent of the applications that were submitted in 2013. According to the National Taxpayer Advocate, dramatic declines in applications for ITINs continued in 2014 and 2015 as a result of these stricter application rules, which have now been codified into law.

What problems are created by the barriers to getting an ITIN?

When the requirements for getting an ITIN are too hard to meet:

1. Immigrants will not be able to get an ITIN and file income tax returns. As a result, they won’t be able to comply with their obligations under federal tax laws.

2. Immigrants who can’t get an ITIN or file tax returns will face problems if they ever become eligible for immigration relief. Certain applications require proof that the applicant has filed tax returns to establish that they have “good moral character.”

3. Immigrants who can’t get an ITIN or file tax returns will also find it harder to prove their work history and that they have been physically present in the U.S. for a certain amount of time, which is also relevant for immigration applications.

4. Low-income immigrants will be prevented from claiming tax supports for which they are eligible, including the Child Tax Credit (CTC), the Additional Child Tax Credit (ACTC), and credits under the Affordable Care Act (ACA). Barriers to obtaining the CTC and ACTC can push low-income children deeper into poverty.

5. If they can’t file tax returns, mixed–immigration status families with members who are eligible for health insurance under the ACA will not be able to prove that they have complied with the individual mandate. And if they received a health insurance premium tax credit, they won’t be able to provide the information about their health insurance and income that the IRS needs in order to reconcile the tax credit that was advanced to them with the tax credit for which they’re actually eligible. This could prevent them from being able to renew their health insurance the following year.

FOR MORE INFORMATION, CONTACT

Tax Partners at 905-836-8755 or email [email protected]

#us tax #ustax #UStaxaccountant #UStaxspecialist #UStaxaudit #ITIN #ITINapplication #ITINrenewal #ITINexpired #1040tax #1040NR #1040IRS #1040Accountant #IRS #IRSphone #IRSaddress #crossbordertax #uscitizentax #IRSobligations #streamline #streamlineprocedure #FBAR #FACTA #TFSAUSCitizen #taxreturnusa #CDNUStreaty #treatytax #OgdenIRS #AustinIRS #Expattax #Expattaxes #CPAexpat #CPAIRS #USTaxService #amnesty #firsttimeabatement #USdilinquenttax #accountant #bookkeeper #payroll #CRAaudit #taxproblem #taxlawyer #taxattorney #USrealestatetax #taxspecialist #CanadianUStaxspecialist #TorontoUStax #NewmarketUStax #MississaugaUStax #BramptonUStax #NorthYorkUStax #ScarboroughUStax #RichmondHillUStax #MarkhamUStax #BarrieUStax #AuroraUStax #HamiltonUStax #VaughanUStax #WoodbridgeUStax #USPassport

Request A Free Consultation

Contact Us

17817 Leslie St, Suite 2

Newmarket, Ontario L3Y 8C6

Tel: (905) 836-8755

Tel: 1-888-TAX-8500

Email: [email protected]